EP Manufacturing Bhd is an investment holding company which engaged in the manufacture, assembly and sale of automotive parts and carbon composite bicycles and bicycles components. The company offers modular assemblies, suspension parts and body and engine parts, as well as engineering plastic parts and lamp assemblies. Its products include body parts, such as cross member, sub frame, dash panel, and door panels; suspension parts, such as trailing arms and link controls; engine parts, such as oil pans; modular assemblies, including corner modules, fuel tank modules, and actuation system for the brake system; engineering plastic parts, such as air ducting, bumper assembly, rear spoilers, and fuel rail assy consisting of fuel rail, injectors, and regulators; and lamp assemblies, including rear combination lamps and head lamps. The Company also involved in the manufacture production, and sale of moulds and dies; manufacture of automotive lamps, allied products, and water meter parts;manufacture, fabrication, production, and sale of engineering plastic components; and manufacture and sale of automotive modular components.

From the above table, we can see that earning of the company is declining since year 2011 from eps 23.90sen to 10.30sen in year 2013. But base on the company share price, the company is still trading at PE below 10.

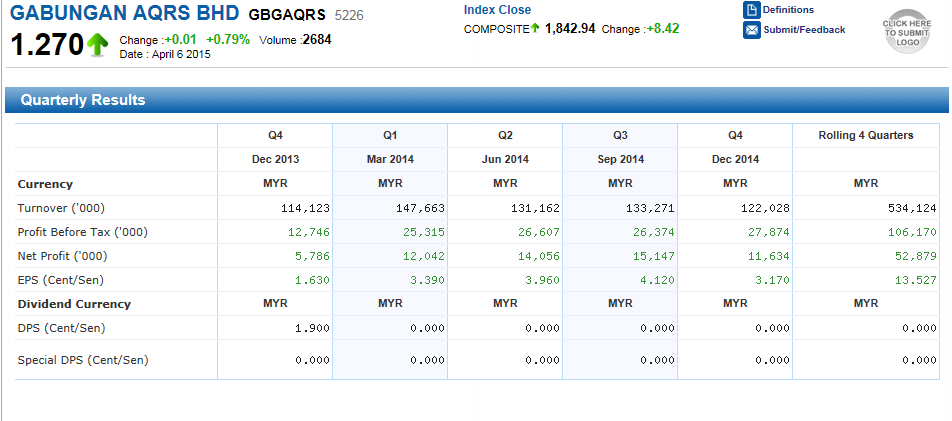

The full year earning of the company in 2014 is 11.255sen, and in the latest quarter result it show 86.67% increased compare to 2013 same quarter. Full year earning also slightly higher compare to earning in 2013 only 10.30sen.

The company show an increasing in earning in the latest result and have a very high NTA of Rm2.13 per shares. The company so far also announced total of 4sen dividend in the past 4 years.

Based on closing price today 81sen, the company PE is 6.91 and Dividend yield of 4.95%

Base on the chart above, we can see that the company price short term up trending since last year December and trying to go above the MA69 line.

From the volume indicator, we also can see that collection has start near end of February this year.

Next quarter result will out on May and normally will come with 2 sen dividend during the month.

Is the company ready to fly back to recent high after break up the MA69 line?

Short Term Target Price: Rm0.94

Happy Trading,

Regards,

Nick